This Video is unable to play due to Privacy Settings.

Error Code: MEDIA_ERR_PRIVACY_SETTINGS

Technical details :

The Video could not be loaded because the privacy settings are disabled. Under the 'Manage Cookies' option in the footer, accept the Functional cookies to allow the video to play.

Session ID: 2022-03-11:54c8618b1429229616728ead Player Element ID: video4108f453fe1043c89acdd6685456dd4c

An insurance application to equally divide assets and pass to the next generation whilst preserving long term family harmony and business continuity.

When planning for distribution of estate, a parent may wish to leave the family business to one or more of their children. It is common for a parent to groom one child to take over their place in the family business. But what happens to the other siblings?

Family businesses face the risk of being dissolved because of disputes over inheritances following the passing of the founder. This is especially true when not all family members are actively involved in the business.

Life Insurance for Estate Equalisation Benefits

To Beneficiaries

Maintains trust and confidence amongst beneficiaries by preventing family dispute over inheritance

Provides financial security for beneficiaries who are not interested in the family business

Provides liquidity to make payment to heirs who are not active in business thus avoiding the need to liquidate the business

Effectively increases the value of the assets that can be distributed among heirs

To the Business

Protects the value of the estate by avoiding the sale of the business

Promotes long-term value creation by minimizing business disruption

Facilitates the continuity and growth of the family business since it does not need to be split between beneficiaries who may not be interested in the business

Supports succession planning

Case Study

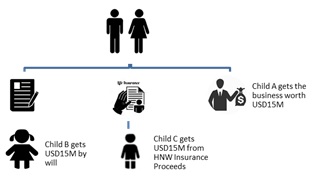

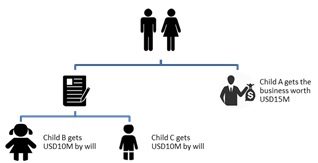

Assume Mr. XYZ, 50 years old, male, has 3 kids. He runs a family business that is worth USD15M and has other accumulated assets worth USD20M. However, only one of his children is interested in inheriting and running the family business.

With Life Insurance

Without Life Insurance

Assume Mr. XYZ buys a HNW Insurance Policy with Sum Assured of USD15M for a Premium of USD5M.

Advantages

Beneficiaries receive Equal Shares

This approach will ensure that each beneficiary receives an amount equal to the value of the business as share of inheritance(i.e. the family business or family assets as applicable).

A life insurance policy is purchased to ensure that the estate is distributed equally whilst ensuring each member of the family is treated fairly.

Beneficiaries receive Equal Amounts

This approach will increase the total estate size so that each beneficiary receives an identical amount based on an assumed future growth.

The members of the family with an interest in running the family business will be able to inherit it, while other members are bequeathed with an equivalent value to the estate derived from the life insurance policy.

Value Creation

Estate equalisation is a very useful application of life insurance in HNW families with more than one intended beneficiary as it allows inheritance to be properly divided equally in an optimal manner. This preserves long term family harmony and unity. For the family business, if there is one, it means business continuity for years and even generations to come.