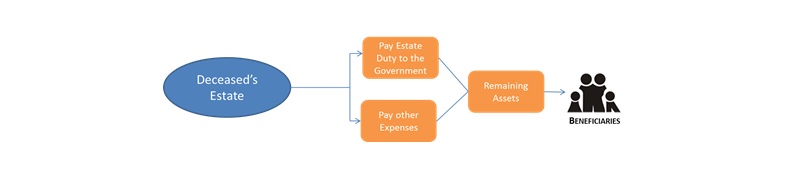

Purchase of a Life Insurance policy to pay some or all of the Estate Duty / Inheritance Tax , can make things easier on the deceased’s family when the need for liquidity arises. One would not be forced to sell assets in distress for the purpose of paying such taxes.

In short, it can give the insured peace of mind that he/she would not be burdening their family and friends with a hefty tax bill when the eventuality has taken place.

The process would involve an individual buying a life policy on his/her life for a face value covering the expected tax liability.

In a jurisdiction where ownership of the policy by the insured would result in proceeds of death benefit falling into his/her estate, there would be a need to consider an alternative ownership structure. Whereas, in some jurisdictions where proceeds of death benefit for a life policy are not captured by Inheritance Tax / Estate Duty, individual ownership is the most appropriate.

As estate and tax planning can be complicated, so the client is best advised to obtain independent legal and tax advice.